Main Street Employers Coalition Statement on Final $900 Billion Covid Relief Package

Main Street Employers

Dec. 19, 2020

Main Street Employers Coalition Statement on Relief Proposal

Main Street Employers

Dec. 14, 2020

Business Coalition Letter on PPP Deductibility

Main Street Employers

Dec. 13, 2020

Survey: Policy Priorities for Main Street Businesses

S Corporation Association

Aug. 31, 2020

Main Street Employers Briefing

Main Street Employers

Oct. 24, 2019

[hr color=”#29545d” style=”line” size=”1px”]The Main Street Employers coalition and the S Corporation Association hosted a Hill lunch on October 24th, 2019. The briefing focused on the pass-through sector and how it has fared under tax reform. Speakers included Senator Steve Daines (MT), Marty Sullivan with Tax Analysts, Bob Carroll with EY, David Winston with the Winston Group, Brian Reardon of S-Corp, and Chris Smith with MSE.

Main Street Employers Coalition Comments on Proposed Section 199A Rules

Main Street Employers

Oct. 1, 2018

[hr color=”#29545d” style=”line” size=”1px”]We are pleased that the proposed rules permit aggregation in a broad range of circumstances. While MSE members have specific concerns with Section 199A and its application under the proposed rules, we are unified that a well-constructed aggregation policy is an essential foundation to putting Main Street businesses on a level playing field with larger C corporations. The following comments include several areas where we believe the aggregation regime could be strengthened and improved.

Whiteboard Video on the Challenges Faced by Main Street Businesses

S Corporation Association

Jan. 14, 2019

[hr color=”#29545d” style=”line” size=”1px”]

Main Street Businesses Briefing Videos

Main Street Employers

Jul. 31, 2018

[hr color=”#29545d” style=”line” size=”1px”]

Statement on Treasury 199A Regulations

By Chris Smith

Aug. 8, 2018

[hr color=”#29545d” style=”line” size=”1px”]The Main Street Employers coalition welcomes Treasury’s guidance applying the new 20% tax deduction to thousands of U.S. businesses organized as pass-throughs—the S-corps, sole proprietorships, and partnerships that comprise 95% of all businesses and who employ the majority of American workers.

EY Study Shows Why Pass-Through Deduction Should Be Broad, Permanent

[hr color=”#29545d” style=”line” size=”1px”]

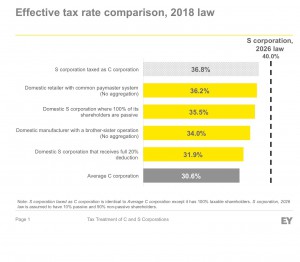

Illustration of tax treatment of C and S corporations under the TCJA

Robert Carroll

EY Quantitative Economics and Statistics Group

Jul. 31, 2018

[hr color=”#29545d” style=”line” size=”1px”] PMSE Comment Letter on New York State SALT FixOverview:

- Examples developed to illustrate the impact of the TCJA on business income taxed under C corporation and S corporation rules

- Effective tax rates (ETRs) developed to capture the major features of the TCJA: 1) 21% corporate tax rate, 2) 20% pass-through deduction for qualified business income (QBI), 3) limitations on deduction for QBI, 4) limitation on deductibility of state and local taxes, and 5) potential issues with aggregation of business entities

- ETRs for S corporations are compared to an average C corporation and to the ETR if the S corporation were instead taxed as a C corporation

Main Street Employers

Jul. 11, 2018

[hr color=”#29545d” style=”line” size=”1px”]The Main Street Employers coalition–representing more than one hundred national business groups and millions of Main Street employers–strongly supports efforts across the states to restore the ability of employers organized as pass-through businesses to deduct their State and Local income taxes (SALT) on their federal tax returns.

PMSE Releases Model State Legislation Preserving Federal, State & Local Tax Deduction for Main Street Employers

Connecticut Paves Way for Other States to Act

Main Street Employers

May 22, 2018

[hr color=”#29545d” style=”line” size=”1px”]Today, the Main Street Employers coalition of national trade groups released model legislation to preserve the federal State and Local Tax Deduction (SALT) for Main Street Employers organized as pass-throughs. This comes on the heels of action by Connecticut last week to become the first state in the country to enact similar legislation, paving the way for other states to act….

Main Street Employers on Tax Overhaul

New Survey Highlights Importance of Guidance in Making Pass-Through Provisions Successful

Main Street Employers

Apr. 17, 2018

[hr color=”#29545d” style=”line” size=”1px”]The Main Street Employers (MSE) coalition released a new survey highlighting the pass-through business community’s initial reaction to the tax Cuts and Jobs Act (TCJA). Early results indicate that the tax relief promised to non-corporate employers is in danger absent clear guidance from IRS and Treasury. Key results include…

Business Community Letter on Aggregation under 199A

Main Street Employers

Mar. 19, 2018

[hr color=”#29545d” style=”line” size=”1px”]As the Treasury Department and Internal Revenue Service drafts rules necessary to implement HR 1, the undersigned organizations request that you use your regulatory authority to adopt a reasonable method of calculating the new 20 percent pass-through deduction to ensure Main Street businesses are not penalized based on how they are organized for business purposes…

Main Street Businesses Deserve Tax Parity With American Corporations

The Hill

By Chris Smith

Feb. 21, 2018 8:00 a.m. ET

[hr color=”#29545d” style=”line” size=”1px”]Now that historic tax reform is done, it’s time for Congress, the Treasury Department and the IRS to work through the details of implementing the new law. For Main Street employers, the stakes couldn’t be higher. As the dust settles, it is becoming clear that there is unfinished business when it comes to tax parity for American employers…

Main Street Employers Group Launches Tax Reform Implementation Effort

Chris Smith Named Executive Director

Focus on Need for Tax Parity for Pass-Through Businesses

Main Street Employers

Feb. 21, 2018

[hr color=”#29545d” style=”line” size=”1px”]Today the Main Street Employers (MSE) coalition, comprised of trade groups representing American Main Street businesses, named Chris Smith as its new Executive Director. Smith is a Washington public affairs veteran and a former Chief of Staff for both the U.S. Treasury Department and the House Ways and Means Committee…

Can Main Street Businesses Just Convert? No!

Nor Should They. Here’s why.

Main Street Employers

Oct. 26, 2017

[hr color=”#29545d” style=”line” size=”1px”]If “corporate-only” advocates have their way and the corporate tax rate is reduced, should pass-through businesses just switch to C status to access the lower rates? Would that shift improve the tax code and how we treat closely-held businesses? The answer to both questions is an emphatic no…

Family Businesses Deserve a Tax Break

‘S corporations’ are major job creators but get a bum rap.

The Wall Street Journal

By Brian Reardon

Oct. 23, 2017 6:46 p.m. ET

[hr color=”#29545d” style=”line” size=”1px”]The U.S. is unique in its prevalence of small and family-owned businesses. S corporations and other pass-throughs employ the majority of workers and are the foundation of thousands of local economies, ensuring that the benefits of economic growth aren’t concentrated in a few financial centers…

Pass-through Businesses: Data and Policy

Tax Foundation: Fiscal Fact

By Scott Greenberg, Analyst

Jan. 2017

[hr color=”#29545d” style=”line” size=”1px”]Key Findings

- The majority of companies in the United States are pass-through businesses. These businesses are not subject to the corporate income tax; instead, their income is reported on their owners’ tax returns and subject to the individual income tax.

- Over the past thirty years, the pass-through business sector has expanded significantly. Pass-through businesses now earn more net income than traditional C corporations and employ the majority of the private-sector workforce…

2016 Main Street Employers Principles Final Letter

Main Street Employers

Mar. 17, 2016

[hr color=”#29545d” style=”line” size=”1px”]Dear Chairmen and Ranking Members:

As Congress debates tax reform to make American businesses more competitive, the undersigned organizations representing employers organized as S corporations, partnerships and sole proprietorships offer the following three principles to help guide your efforts…

Ending the One-Two Corporate Tax Punch

Jason Furman is right about the ‘stupid’ policy on overseas income. Domestic policy also isn’t so bright.

The Wall Street Journal

By Brian Reardon and Tom Nichols

Feb. 25, 2016 7:21 p.m. ET

[hr color=”#29545d” style=”line” size=”1px”]We don’t often agree with President Obama’s chief economist, Jason Furman, but he got it exactly right when he noted earlier this month that the U.S. treatment of international business income is a “stupid territorial tax system…”

An Overview of Pass-through Businesses in the United States

Tax Foundation: Special Report

By Kyle Pomerleau, Economist

Jan. 2015

[hr color=”#29545d” style=”line” size=”1px”]Key Findings

- Pass-through business income is taxed on the business owners’ tax returns through the individual income tax code.

- Pass-through business income faces marginal tax rates that exceed 50 percent in some U.S. states.

- Pass-through businesses face only one layer of tax on their profits compared to the double taxation faced by C corporations…