The Importance of Section 199A

Section 199A was enacted to ensure pass-through businesses (S corporations, sole proprietorships, and partnerships) can compete with their larger publicly-owned competition by giving them a deduction equal to 20% of their qualified business income.

The provision serves two primary purposes: 1) encourage job creation and economic growth by reducing the tax burden on pass-through businesses, and 2) maintain tax parity between pass-throughs and C corporations, which face a much lower 21% rate.

While the corporate rate is permanent, Section 199A expires at the end of 2025, threatening millions of small businesses with massive tax hikes that will threaten their very existence.

Enacting the Main Street Tax Certainty Act is the Main Street Employers Coalition’s #1 priority. This bipartisan, bicameral effort is led by Sen. Steve Daines (S. 1706) and Rep. Lloyd Smucker (H.R. 4721) and enjoys the support of dozens of lawmakers, including the entire Republican membership of the Ways & Means Committee.

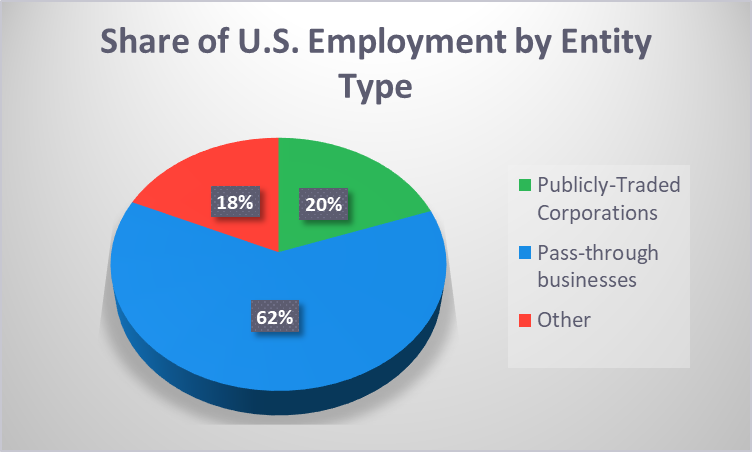

Main Street businesses are bigger than big business. They employ more workers, and they contribute more to our national income. While public corporations employ just under 20 percent of the private sector workforce, private companies employ more than 80 percent. Of those private companies, pass-through businesses who depend on the 199A deduction employ more than 62 percent of the American private-sector workforce.

The employment story has geographical implications as well. According to EY, private company employment is spread evening across the country (green), providing much needed jobs and opportunity to sections of the country that would otherwise lack an economic base. Meanwhile, the smaller share of public company employment tends to be concentrated in city centers and on the coasts. If not for a robust Main Street sector, more communities would see less opportunity and more boarded up buildings.

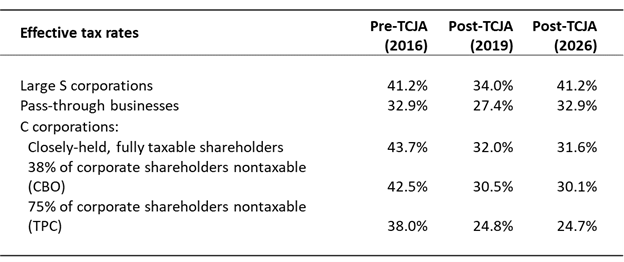

The Section 199A deduction is critical when it comes to maintaining rough tax parity between business types. A recent EY study shows that publicly-traded C corporations pay effective rates somewhere between 25 and 31 percent, while pass-throughs businesses pay between 27 and 34 percent. Large pass-through businesses – those in danger of seeing their taxes raised – already pay 34 percent with the 199A deduction, well above the effective rate of their public competition.

How Does Section 199A Work?

If Section 199A is allowed to expire, Main Street businesses will be forced into a Hobson’s choice – remain in their pass-through form and pay rates 16 percentage points higher than the competition or convert to C status and be forced into the double tax.

Don’t publicly-traded companies already face the same double tax? Not exactly. In recent years, the percentage of C corporation shareholders who are tax advantaged – they either pay no taxes at all (charities, endowments) or pay greatly reduced rates (qualified retirement accounts, foreign shareholders) — has increased dramatically. In the sixties, four out of five shareholders paid the full tax. Today, the Tax Policy Center estimates that three out of four pay no tax or greatly reduced rates.

The EY study referenced above addresses this variable by providing alternate results depending on competing profiles of shareholders. So a C corporation with fully taxable shareholders (say an S corporation that converted to C) would pay an effective rate of 32 percent, while a public company with 75 percent tax-advantaged shareholders would pay only 25 percent. That’s a huge difference and it suggests the old corporate double tax is of decreasing importance when measuring the tax burdens of public companies.